Recent disruptions in the global food supply chains have highlighted Africa's urgent need to become self-sufficient in food production. Traditionally, the continent has turned to small-scale community-based agricultural projects as a means to meet its food needs. But feeding a population of more than 1.2 billion people requires more than communal farming; it calls for a paradigm shift toward agriculture on an industrial scale. Our milestone tenth edition of Africa Focus opens with an article exploring obstacles to large-scale farming in Africa and how they may be overcome to secure funding required for such agricultural megaprojects.

While Angola has entered an ambitious plan to diversify its economy, it remains heavily dependent on its oil & gas industry. Hydrocarbon revenues are crucial for funding Angola's commitments under the Paris Agreement, but also for diversifying the country's economy and improving the livelihoods of its citizens. Our second article looks at the latest developments in Angola's oil & gas sector, including increased M&A activity and a three-well offshore exploration project at a depth of 3,628 meters (11,903 feet) below mean sea level—a new world record water depth set in 2021.

Africa is home to many of the world's most biodiverse regions, including eight of the 36 recognized global biodiversity hotspots. The Congo rainforests have also overtaken the Amazon as the most significant carbon sink on Earth. Our third article highlights the scale of the challenge of biodiversity protection in Africa and options to fund it.

Trade ties between Africa and the United States are seeing something of a revival as the US seeks to revitalize its economic engagement on the continent. The US African Growth and Opportunity Act (AGOA) is one such pivotal agreement that is due to go before the US Congress in 2025.

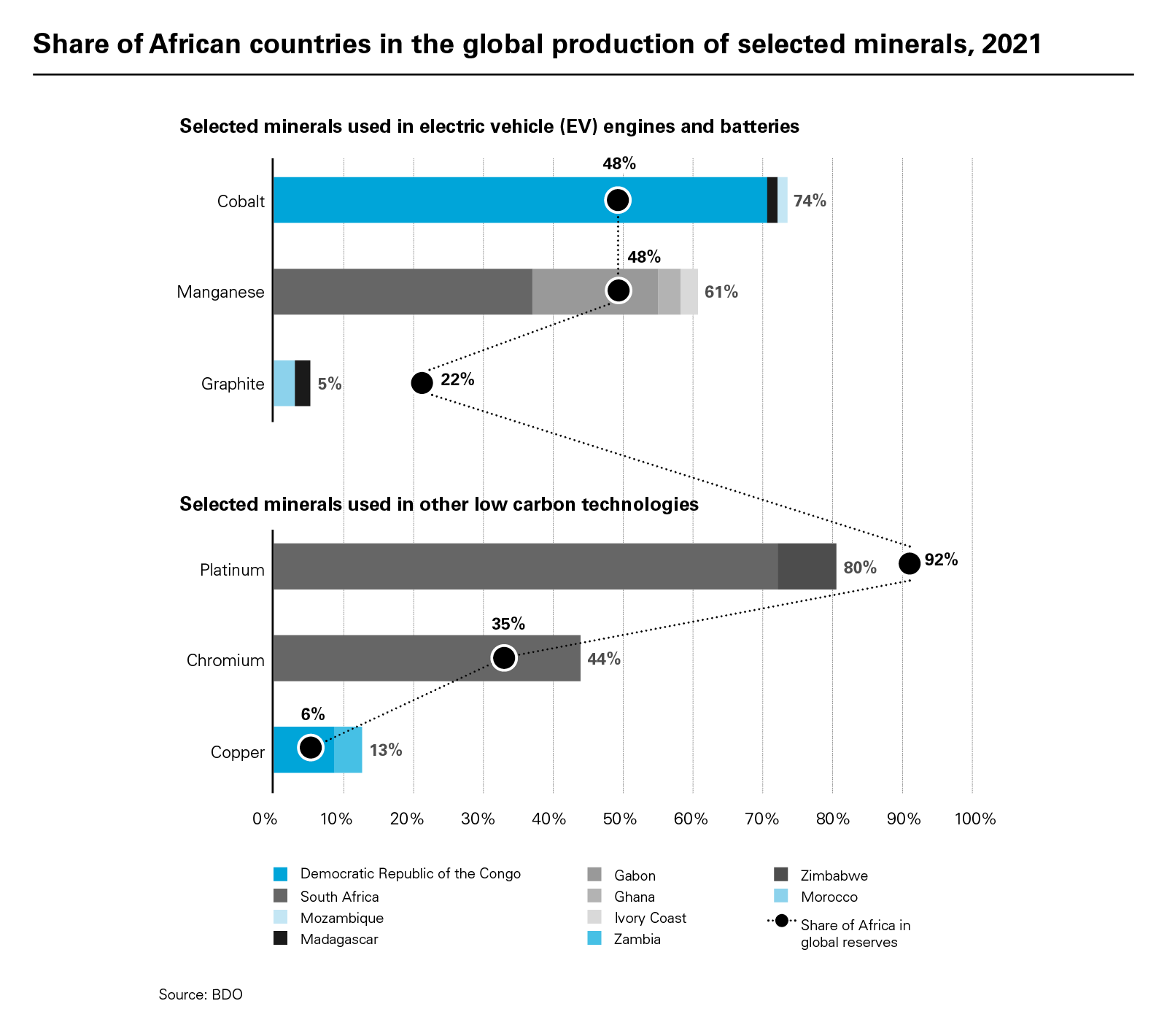

Africa holds a remarkable 30 percent of the world's mineral reserves, yet it only accounted for less than 10 percent of global mining exploration spending and less than 5 percent of the sector's global revenue in 2022. Many of Africa's minerals are vital for reducing carbon emissions and transitioning to renewable energy. Developing these reserves sustainably is crucial for Africa's economies. Our final article examines how mining companies across Africa continue to find financing for the development of their projects.

Africa's agricultural revolution: From self-sufficiency to global food powerhouse

Don't let a crisis go to waste: Financing mining & metals projects in Africa in 2023

Financing new mines is and always has been a risky business. Long project timelines, price volatility, navigating political conditions, ESG risks and more are now colliding with rising interest rates and fears of a global economic downturn. Yet, amid geopolitical crisis and economic uncertainty, mining companies across Africa continue to find financing for the development of their projects.

Mining & metals projects across Africa are benefiting from a sea change driven by the COVID-19 pandemic, acceleration of the energy transition and Russia's invasion of Ukraine. Critical minerals and the mining sector more broadly have become part of energy security policies across developed markets. Industries buffeted by supply chain disruptions and ESG pressures also seek their own security, too, directly investing in or partnering with miners to secure supply.

Though the continent is home to as much as 30 percent of the world's mineral reserves, as of 2022 it accounted for less than 10 percent of global mining exploration spending and less than 5 percent of the sector's global revenue. Africa's mineral wealth has therefore emerged as a key theatre in the race to secure the supplies needed to achieve decarbonization.

Capital that has traditionally flowed into African oil & gas projects is now being redirected into mining, as funders adapt their portfolios in response to the energy transition

In 2022, there's been an uptick of interest in smaller mining projects that point to larger changes occurring across the sector and region. Junior miners in Africa typically struggle to finance new projects because of the risks involved. They hold few assets, their exposure to commodity prices is highly concentrated, it can be difficult to establish the value of early-stage projects and they're often comparatively unproven to lenders and potential partners. But even with tightening financial conditions, capital providers seem eager for the return that smaller mining projects generate, especially those producing critical minerals or high-grade iron ore.

Some of the shift in risk appetite is structural. Major mining companies have not invested significantly in exploration and development for the past decade. Now they're playing catch-up. Majors have begun participating in venture capital investments meant to accelerate the deployment of innovative technologies and finance exploration with junior miners. Firms are returning to Africa because of its immense untapped exploration potential. BHP, which exited its African assets in 2014, has acquired a 17 percent interest in Kabanga Nickel, a subsidiary of Lifezone Metals, which owns the Kabanga project in Tanzania.

Given the relative retrenchment of major miners and the significant cost of large M&A transactions, the near certainty of rising demand for most minerals is pushing investors to proactively seek out nascent, smaller projects in Africa to develop. This includes surging interest from startups linked to the tech world looking to secure long-term supply for the energy transition, for example, KoBold Metals, which announced plans to commit US$150 million to develop the Mingomba copper-cobalt mine in Zambia at the US-Africa Leaders Summit last December. Industrial manufacturers and metals firms have every reason to invest directly into small projects alongside junior miners if it helps efforts to reduce emissions across the value chain and target higher-grade finds to source ores that require less energy to beneficiate and refine in the first place. And we are seeing them do so using an array of structures ranging from traditional equity to royalties and streams to pre-pay financing—all (of course) paired with a substantial long-term offtake.

Capital's energy transition

30%

Africa is home to about 30 percent of the world’s mineral reserves

The sector has traditionally not been associated with green financing, given historic ESG issues associated with many mining & metals operations, but acknowledgment of the crucial role the sector has to play in the energy transition is changing this dynamic. For example, Egyptian gold miner Centamin was recently able to access a US$150 million sustainability-linked revolving credit facility from a group of commercial bank lenders, a first for the country's mining sector. Interest in similar financing arrangements is steadily rising.

At present, there is no unified ESG framework to assess the impact of mining & metals projects. We expect this to shift as the sector becomes more vertically integrated within itself and with other industries. The Simandou iron ore project and smaller iron ore projects in sub-Saharan Africa producing high-grade ores can help steelmakers taking on sustainability-linked debt or facing regulatory pressures to minimize emissions and consume less electricity when running electric arc furnaces. Other miners are seeking opportunities to enter into value chains with hydrogen or combining project development with investments in renewable energy infrastructure, which may open up additional financing options in the years ahead.

Finally, capital that has traditionally flowed into African oil & gas projects is now being redirected into mining, as funders adapt their portfolios in response to the energy transition. High interest rates have similarly driven investors away from industries such as tech that have traditionally relied on loose financial conditions to finance rapid growth. Africa's wealth of unexplored and undeveloped mineral reserves has allowed miners to weather difficult economic and political conditions better than expected.

Security first

5%

As of 2022, Africa accounted for less than 5 percent of the global mining revenue

More interesting in the longer term, however, is the shifting political environment and its effect on investor preferences as well as lenders and investor mandates. US Undersecretary for Economic Growth, Energy, and the Environment Jose W. Fernandez attended the Mining Indaba in mid-February, noting "we don't have enough critical minerals to power the world's clean energy agenda, but our current supply chains for these minerals—from extraction to production to recycling—are simply not diverse enough for the energy future that's coming." US Treasury Secretary Janet Yellen is currently leading efforts with US allies to reform the World Bank and reorient its mission toward combatting climate change while supporting development, part of an expanding push in many developed markets to leverage existing trade finance or development institutions to more actively support critical minerals projects.

Anxieties about dependence on China's mining & metals complex are upping the pressure on export credit agencies, development financial institutions and commercial banks to lend into the mining sector to secure alternative sources of supply. The United States' Mineral Security Partnership—a program launched last June with the participation of 12 partner countries and the EU—aims to promote ethical mining practices across the sector's value chain in parallel with developing EU efforts to reform mine and refinery permitting processes and launch a central purchasing agency for critical minerals. Considerable amounts of political capital are being spent on efforts to spur investment that comports with climate concerns and more rigorous ESG standards as a matter of geopolitical competition and security, not only return on investment or risk management.

Promoting investment into the mining & metals sector on the continent provides jobs and revenues, and acts as a disincentive to migratory pressures

At the same time, Chinese investors are taking advantage of the easing of COVID-19 restrictions and racing to secure critical mineral supply chains. Investors and miners from China generally have a higher risk tolerance, as well as the financial and technical capacity to advance projects quickly. Governments are also looking to leverage their existing relationships with Chinese firms to extract more value. The Democratic Republic of the Congo has been a salient example, as President Felix Tshisekedi looks to renegotiate deals signed in 2008 to increase Chinese investment into infrastructure and ensure that local labor is used for construction. In other areas, Chinese investors had a definitive edge as they're already on the ground. For instance, seven of nine of the existing large or more developed lithium projects across the continent are partially or completely Chinese owned.

Security factors are also at play. Promoting investment into the mining & metals sector on the continent provides jobs and revenues, and acts as a disincentive to migratory pressures. The European Investment Bank (EIB) and European Bank for Reconstruction and Development (EBRD), for example, both have active programs to provide equity and/or debt to projects on the continent. Sub-Saharan Africa alone hosts more then 18 million refugees and more than 14.2 million internally displaced people. The continent's relative youth—20 percent of Africa's population is between the ages of 15 and 24 years and comprises more than half of its workforce—poses significant problems for countries struggling to create enough new, paying jobs. Mining projects bring jobs and infrastructure investment, providing governments with new avenues to promote domestic refining and metals production for "green" supply chains. Building up metals production, especially when coupled with investments into renewable energy supplies and green hydrogen production, then creating an industrial base with considerable forward and backward links across supply chains will generate high levels of indirect employment and support greater economic complexity and diversification.

As tensions between the collective "West," Russia and China intensify, along with pressures to decarbonize, so will the race to secure financing for new projects and development across Africa. Africa's mining & metals sector stands to benefit.

Special thanks to Nick Trickett, Business Development Manager for the Mining & Metals Industry Group, for his assistance with this article.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Share of African countries in the global production of selected minerals, 2021 (PDF)

View full image: Share of African countries in the global production of selected minerals, 2021 (PDF)